Market Scenario

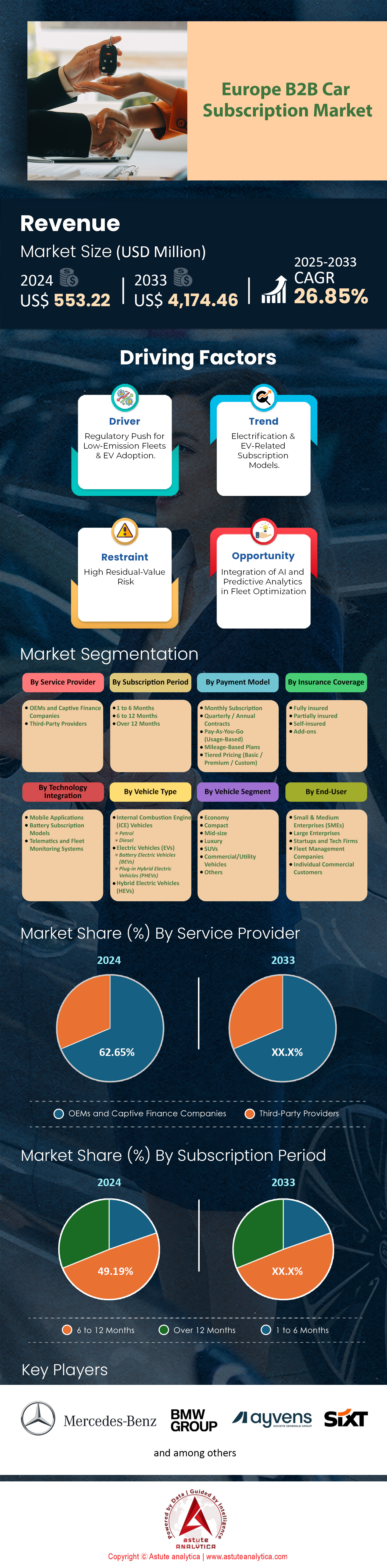

Europe B2B car subscription market size was valued at US$ 553.22 million in 2024 and is projected to hit the market valuation of US$ 4,174.46 million by 2033 at a CAGR of 26.85% during the forecast period 2025–2033.

Key Findings in Europe B2B Car Subscription Market

- Based on service Provider, OEMs and Captive Finance Companies segment holds highest share 62.65%(2024).

- Based subscription period, 6 to 12 Months segment holds highest share 49.19% (2024).

- Based on payment model, Monthly Subscription segment holds highest share 44.11% (2024).

- Based on insurance Coverage, Fully insured segment holds highest share 56.31% (2024).

- Based on technology, integration, Mobile Applications segment holds highest share 50.56% of the Europe B2B car subscription market (2024).

- Based on vehicle type, Internal Combustion Engine (ICE) Vehicles segment holds highest share 66.97% (2024).

- Based on vehicle segment, SUVs segment holds highest share 24.63% (2024).

- Based on end users, Large Enterprises segment holds highest share 38.84% (2024).

- Germany is powerhouse in the regional market with revenue contribution of over 23.63%.

The Europe B2B car subscription market has matured into a critical mobility pillar, valued at USD 553.22 million as of 2024, reflecting a year-on-year growth rate of nearly 27%. This surge is fueled by corporate desires to decouple mobility from asset depreciation, specifically regarding Electric Vehicles (EVs). The total active subscription fleet across Europe has reached 920,000 vehicles, with EVs now constituting 48% of all B2B active contracts as of 2025—a sharp rise from just 28% in 2023.

The average subscription duration has settled at 10 months, striking a balance between the rigidity of 36-month leases and the high cost of daily rental. Fleet utilization rates are optimizing at 94%, driven by algorithmic asset allocation that minimizes idle time. Corporates are seeing clear financial incentives: the shift to subscription models is generating average operational savings of 12% compared to traditional leasing when factoring in administrative reduction, insurance stability, and residual value risk avoidance.

To Get more Insights, Request A Free Sample

Which Nations are Leading the Usership Revolution in Europe’s B2B Car Subscription Market?

Germany remains the undisputed heavyweight, commanding a 23.63% market share. The concept of "Auto-Abo" is fully integrated into German corporate procurement, where 60% of SMEs now list subscription as a standard sourcing channel.

The United Kingdom follows closely in innovation, if not total volume, recording the highest growth rate at 28% YoY. This is largely driven by Salary Sacrifice schemes, which have seen a 65% increase in uptake among corporate employees due to favorable Benefit-in-Kind (BiK) rates.

France’s Europe B2B car subscription market is heavily regulated-driven. With the Loi d’Orientation des Mobilités (LOM) imposing strict quotas, the French B2B subscription sector holds an 18% market share, but notably, it boasts the highest EV concentration at 58% of the subscribed fleet.

Belgium has become a unique outlier; due to tax reforms effectively ending deductibility for ICE vehicles, 94% of new B2B subscriptions in Belgium are electric. Conversely, Spain is carving a niche in logistics, witnessing a 15% growth specifically in Light Commercial Vehicle (LCV) subscriptions, outpacing passenger car growth in the region.

Who Dominates the Competitive Landscape in 2025?

The Europe B2B car subscription market is bifurcating between massive incumbents and agile tech platforms. Ayvens (the entity formed from ALD and LeasePlan) retains dominance with a 16% market share, leveraging its massive existing fleet to offer flexible terms. However, pure-play tech challenger Finn has scaled aggressively, now managing over 40,000 active subscribers, primarily in Germany and the US, by digitizing the entire onboarding process to under 24 hours.

On the other hand, Mercedes Benz has emerged as most dominant in the regional market with market share of nearly 12.92% in terms of OEM. However, Chinese OEMs are disrupting the pricing structure. Brands like BYD and Nio have captured 12% of the total B2B subscription volume by offering rates 15-20% lower than European legacy peers, absorbing tariff impacts to gain market foothold. Meanwhile, Volvo’s ‘Care by Volvo’ remains the benchmark for OEM-led programs, retaining high retention with a 72% renewal rate among corporate clients. The market also witnessed consolidation, with five major M&A deals in 2025 alone as leasing giants acquired regional subscription startups to secure tech stacks.

What Vehicle Segments are Driving Corporate Demand?

While passenger vehicles still dominate volume in the Europe B2B car subscription market, the Light Commercial Vehicle (LCV) segment is the fastest-growing category, expanding by 19% in 2025. This is driven by "Project-Based Fleets"—construction and logistics firms subscribing to vans for specific 6-9 month contracts.

In the passenger segment, the "Budget Green" category—utilizing 3-4 year old refurbished EVs—has emerged as a vital tier, costing roughly 35% less than new assets. This segment is popular for junior staff mobility. Conversely, premium EV subscriptions (e.g., Porsche Macan EV, Tesla Model S) face supply constraints, with waiting lists averaging 2 months despite the flexibility promise.

Battery technology also influences segmentation. For urban delivery fleets, vehicles equipped with LFP batteries are preferred by 70% of logistics managers due to their durability in high-cycle charging environments.

Why are Regulatory and Economic Pressures Catalyzing Growth?

Financial volatility is the primary accelerant in the Europe B2B Car subscription Market. With commercial fleet insurance premiums rising by 25% in the UK and Southern Europe, SMEs are flocking to bundled subscriptions where insurance costs are fixed and shielded from annual spikes. Furthermore, the persistent high-interest environment has increased traditional leasing costs by approximately 15%, narrowing the price gap and making the flexibility premium of subscriptions mathematically negligible.

Regulatory compliance is equally forceful. The enforcement of Euro 7 standards has added approx €2,000 to the cost of purchasing new diesel vans, pushing small businesses toward OPEX-based subscriptions to avoid this CAPEX shock. In cities like Amsterdam and Oxford, 100% of construction fleets entering Zero Emission Zones (ZEZ) are now subscribed rather than owned, as firms refuse to buy assets useful only for specific city-center contracts.

How Are Digital Innovation and MaaS Integration reshaping Usage?

The user experience is now entirely digital in the Europe B2B car subscription market. 100% of leading providers utilize "KYB" (Know Your Business) automated checks, slashing approval times from weeks to hours. Telematics integration is deepening; 85% of fleet managers now utilize "Privacy Mode" features to ensure GDPR compliance for employees during non-working hours.

Mobility-as-a-Service (MaaS) integration has moved beyond buzzwords. 20% of large corporate contracts now include "Multi-Modal Bundles," where a single subscription invoice covers a company car, an e-bike, and public transport credit.

As per recent market analysis of the Europe B2B car subscription market, innovation extends to revenue models. Vehicle-to-Grid (V2G) pilots in the Nordics involve 5% of the subscription fleet, generating rebates that lower monthly fees for companies willing to keep cars plugged in during peak grid stress. Additionally, Over-the-Air (OTA) feature unlocking allows companies to pay for heated seats or autonomous driving aids only during winter months or long trips, reducing base monthly costs.

What Risks and Opportunities Lie Ahead for Fleet Managers in the Europe B2B Car Subscription Market?

The most significant risk managed by subscriptions in 2025 is Residual Value (RV) collapse. With early-generation EVs seeing resale values drop by up to 40%, subscription providers are effectively functioning as "risk insurers," absorbing this depreciation shock. This has made the Total Cost of Usership (TCU) the defining metric, replacing TCO.

Opportunities are abundant in the "Second-Life" market. Providers in the Europe B2B car subscription market extending vehicle lifecycles to 48 months (re-subscribing the same asset 3-4 times) are seeing profit margins increase by 15% on older assets. For corporates, the biggest opportunity lies in “Flex-Up” capacity; retail logistics firms now routinely expand fleets by 25% during Q4 peaks and contract them in Q1, a dynamic impossible with traditional leasing.

Who Are the Primary End Users?

Currently, large enterprises are dominating the market but SMEs remain the volume engine, accounting for 31% of total revenue of the Europe B2B car subscription market, driven by the need to preserve credit lines for working capital. However, Large Enterprises are the fastest adopters of "Corporate Car Sharing," where 1 in 5 major firms has replaced assigned cars with a pooled subscription fleet, reducing total vehicle count by 20%.

The "Expat Mobility" segment is also robust, with 90% of multinational assignments (1-2 years) now serviced via subscriptions to match visa tenures perfectly. Finally, the Last-Mile Delivery sector consumes 18% of all subscriptions, exclusively utilizing electric vans to maintain urban access and hit carbon reduction targets of 20% per fleet instantly.

Segmental Analysis

Leveraging Massive Fleet Inventory and Captive Financial Power For Market Control

The OEMs and Captive Finance Companies segment holds highest share 62.65% in the Europe B2B car subscription market because automakers utilize existing supply chains to undercut third-party pricing. Manufacturers like Stellantis aggressively allocate over 220,000 vehicles to their Free2Move platform, bypassing dealership delays that plague independent leasing firms. KINTO by Toyota has expanded its fleet to exceed 100,000 units across Europe, securing dominance by offering diverse mobility tiers directly to corporate clients. These captives leverage balance sheets to absorb vehicle depreciation risks, which can hit USD 3,500 annually per unit, a cost independent startups cannot sustain. Volvo’s dedicated Care by Volvo service now manages over 30,000 active subscriptions, effectively converting traditional lease customers into subscribers.

- Sixt+ ordered 250,000 Stellantis vehicles to bolster premium subscription availability.

- Lynk & Co amassed 170,000 members by prioritizing subscription-only access models.

- Hyundai’s Mocean subscription service recently expanded operations into the German market.

Automakers invested over USD 1.2 billion in 2023-2024 to build direct-to-consumer digital infrastructure, creating a barrier to entry for smaller providers. Mercedes-Benz focuses its high-end subscription operations in Germany, Italy, and Switzerland, capturing the luxury corporate sector. OEMs prioritize their subscription channels during shortages, adding approximately 300,000 new units to these fleets last year alone. Financial strength allows them to offer rates USD 100 lower monthly than competitors. Consequently, the Europe B2B car subscription market relies heavily on these dominant players for consistent vehicle access.

Bridging Corporate Probation Periods With Strategic Medium Term Contract Flexibility

Since the 6 to 12 Months segment holds highest share 49.19% in the Europe B2B car subscription market, businesses predominantly use these terms to align with standard employee probation timelines. German labor laws mandate a 6-month probation period, compelling companies to utilize subscriptions rather than committing to 3-year leases for new staff. Similarly, UK-based firms face probation windows of 3 to 6 months, driving demand for 6-month rolling contracts that carry no early exit penalties. Standard factory delivery times for new fleet vehicles currently span 9 to 14 months, forcing fleet managers to rely on 6-12 month subscriptions as interim mobility solutions.

- Sixt+ restricts short-term rentals to 120 days, pushing users to 6-month plans.

- Corporate fleet vehicles average 49,680 miles over three years requiring durable solutions.

- Mocean encourages 6-month renewals by allowing vehicle swaps only after this duration.

Cost structures further validate this dominance in the Europe B2B car subscription market, as 6-month subscriptions average USD 550 per month, offering substantial savings over daily rental rates. Corporate consulting projects across Europe average 4 months but frequently extend, making the 12-month cap a safe operational buffer. "Mini-lease" products specifically target this 3 to 12-month window to bridge the gap between daily hire and long-term leasing. Cancellation notices are typically just 1 to 3 months, providing liquidity advantages during economic downturns. Therefore, the European market thrives on this tenure for its perfect operational alignment.

Eliminating Capital Expenditure Through Comprehensive and Predictable Monthly Billing

As the Monthly Subscription segment holds highest share 44.11%, the Europe B2B car subscription market is driven by corporate preferences for all-inclusive operating expense models over capital expenditures. A standard monthly fee, averaging USD 550 to USD 650, bundles insurance, maintenance, and road tax, delivering an estimated annual value of USD 1,300 that fleet managers need not process separately. Subscribers effectively outsource asset risk, avoiding steep depreciation costs that often exceed USD 3,200 in a vehicle's first year. Lynk & Co exemplifies this appeal with a flat monthly rate of around USD 690, simplifying complex corporate budgeting processes.

- Upfront deposits are rare, often set at USD 0 or one month’s fee.

- Contracts include generous usage allowances typically set at 1,250 kilometers monthly.

- Administrative activation fees average USD 215 but are frequently waived promotionally.

Operational agility allows businesses to adjust fleet sizes with only one month's notice, responding instantly to project fluctuations. Excess mileage is billed transparently between USD 0.11 and USD 0.22 per kilometer, preventing unexpected end-of-term penalties. Insurance inclusion alone saves companies approximately USD 880 to USD 1,100 annually per vehicle in administrative sourcing costs. Such friction-free financial architecture is crucial for modern businesses prioritizing cash flow. This flexibility cements the monthly model as the backbone of the Europe B2B car subscription market structure.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Mitigating Range Anxiety and Infrastructure Deficits With Combustion Engines

Internal Combustion Engine (ICE) Vehicles holds highest share 66.97% in the Europe B2B car subscription market because corporate fleets demand range reliability that electric infrastructure cannot yet guarantee. Europe currently operates only 630,000 public charging points against a 2030 requirement of 8.8 million, creating severe operational risks for business travelers. Real-world data indicates a diesel vehicle saves approximately USD 58 in fuel costs compared to public EV charging for a Berlin-to-Madrid trip. High-mileage corporate users, averaging 30,000 kilometers annually, depend on the 400km+ range advantage diesel engines hold over standard electric models.

- Residual values for 3-year-old ICE vehicles remain strong at over 55%.

- EV residual values dropped to roughly 44% increasing their subscription premiums.

- Corporate fleet CO2 emissions average 138 g/km reflecting continued heavy ICE usage.

Fleet managers also prefer ICE models to avoid the financial volatility associated with dropping EV residual values. Hundreds of diesel variants are immediately available for subscription, whereas electric estate cars suitable for equipment transport remain scarce. Diesel engines still comprised a significant majority of new fleet registrations in 2024 due to these practical constraints. Until charging networks achieve density comparable to petrol stations, ICE superiority will persist. Thus, the Europe B2B car subscription market remains anchored by traditional powertrain technology.

To Understand More About this Research: Request A Free Sample

Top Players in the Europe B2B Car Subscription Market

- BMW Group

- Mercedes-Benz Group AG

- Stellantis N V

- Sixt SE

- Avis Rent A Car System, LLC

- Budget Rent A Car System, Inc.

- ALD AutoLeasing D GmbH

- Hertz Corporation

- Volkswagen

- Carvolution

- Lizy

- Other Prominent Players

Market Segmentation Overview

By Service Provider

- OEMs and Captive Finance Companies

- Third-Party Providers

By Subscription Model

- 1 to 6 Months

- 6 to 12 Months

- Over 12 Months

By Payment Model

- Monthly Subscription

- Quarterly / Annual Contracts

- Pay-As-You-Go (Usage-Based)

- Mileage-Based Plans

- Tiered Pricing (Basic / Premium / Custom)

By Insurance Coverage

- Fully insured

- Partially insured

- Self-insured

- Add-ons

By Technology integration

- Mobile Applications

- Battery Subscription Models

- Telematics and Fleet Monitoring Systems

By Vehicle Type

- Internal Combustion Engine (ICE) Vehicles

- Petrol

- Diesel

- Electric Vehicles (EVs)

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Hybrid Electric Vehicles (HEVs)

By Vehicle Segment

- Economy

- Compact

- Mid-size

- Luxury

- SUVs

- Commercial/Utility Vehicles

- Others

By End User

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- Startups and Tech Firms

- Fleet Management Companies

- Individual Commercial Customers

By Region

- The UK

- Germany

- France

- Italy

- Spain

- Poland

- Russia

- Rest of Europe

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |